Doesn't matter if they would do it or not. They have the money available. Foster studios, make partnerships. If Apple, Sony and Nintendo can do it, why can't MS?There's no guarantee that they would spend that $70B on Xbox and gaming. They're trying to acquire ABK, first and foremost for King and mobile gaming because they don't exist in that market. Having King along with Diablo Immortal and COD mobile gets their foot through the door to where they could even have their own mobile storefront to compete with Apple and Google which IS a good thing. The more competition there is, the better it is for everyone.

They built a studio from the ground up with The Initiative and hired way too many "higher" people who thought they were the boss when they weren't. How did that work out? It's simply far better and easier to acquire a company that it already set as opposed to building it from the ground up.

Microsoft has made good to great games this generation but don't seem to count because it's not what you want them to be. I have only had two games thus far - Halo Infinite and Hi Fi Rush. Both for me are great games but Forza, Flight Sim, etc. are great games as well but do they not count because they're not for me? In that scenario, since Nintendo isn't for me, I guess every game they release is trash if we're going based on "is the game for me".

Microsoft's acquisition of Activison Blizzard

- Thread starter Darth Vader

- Start date

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

You post is very clever and can be used to every Xbox generation.You're one of the few here that doesn't want Xbox to die then as that's all I ever read here. That and more topics/posts about Xbox than PlayStation which is weird to me for a forum that is 99% PlayStation centered and focused. I want Microsoft to do better too but wanting that and it actually happening are two very different things.

Yeah, we've had discussions regarding the Xbox consoles. The Xbox Series X is literally used for their server blades so the consoles going away is highly unlikely. I disagree with your opinion regarding the consoles because you want them to be more like PC's including the price. How would being $1000 help them sell more consoles? It wouldn't.

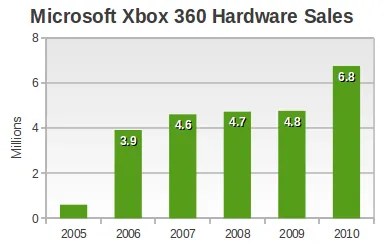

Their hardware business was down 30% but why is that even a surprise? First, they haven't had a major AAA title since Halo Infinite and second, they're literally using the Series X for their server blades which to be honest, I would do the exact same thing right now because why have consoles sitting on store shelves when I don't have a major AAA title to market it with? All their other aspects increased which considering the 2022 year they just had, I would say that's better than expected and Microsoft expected worse for the quarter.

Not only that but people are acting like we're a decade into the generation when we're only 2 1/2 years in. We all know that Microsoft has fucked up a few times this generation but Xbox One was far worse and Microsoft has been trying to get out of that disaster or years. We all know it doesn't happen overnight.

Microsoft is already shifting away from consoles being their main focus. It's simply an option. One that should always be there for those like me who want it but to eliminate it or overprice it isn't going to make it better at all. It would make it worse. Microsoft's current business model is better than the traditional business model because it didn't work for three generations so why would they stay with it for a fourth generation? That would make no sense.

Like I said before, im giving Microsoft this entire generation to see how it all plays out. You can't pivot on a whim. You have to build it all up first and that in of itself takes time. Switching business models would only set them back further and makes things even worse than they already are.

So why they didn't change ever after 20 years?

Why do you keep giving Xbox one more chance? Again giving MS "this entrie generation to see how it all plays out".

MS don't want to lern and adapt to what the gaming market wants... they want to dominated it the easy way... buying their place without giving option for competition.

At least 20 years ago MS tried to release some games... today not even that anymore.

They just don't care about gaming.

You are too médiocre to waste more time on youI don't need to fool anyone. I say exactly what I am and if people don't like it, that's their problem, not mine. *shrugs*

Do I wan't Xbox to die? Sure, but if Hitler was alive I would also want him to die. Am I wrong?You're one of the few here that doesn't want Xbox to die then as that's all I ever read here. That and more topics/posts about Xbox than PlayStation which is weird to me for a forum that is 99% PlayStation centered and focused. I want Microsoft to do better too but wanting that and it actually happening are two very different things.

Yeah, we've had discussions regarding the Xbox consoles. The Xbox Series X is literally used for their server blades so the consoles going away is highly unlikely. I disagree with your opinion regarding the consoles because you want them to be more like PC's including the price. How would being $1000 help them sell more consoles? It wouldn't.

Their hardware business was down 30% but why is that even a surprise? First, they haven't had a major AAA title since Halo Infinite and second, they're literally using the Series X for their server blades which to be honest, I would do the exact same thing right now because why have consoles sitting on store shelves when I don't have a major AAA title to market it with? All their other aspects increased which considering the 2022 year they just had, I would say that's better than expected and Microsoft expected worse for the quarter.

Not only that but people are acting like we're a decade into the generation when we're only 2 1/2 years in. We all know that Microsoft has fucked up a few times this generation but Xbox One was far worse and Microsoft has been trying to get out of that disaster or years. We all know it doesn't happen overnight.

Microsoft is already shifting away from consoles being their main focus. It's simply an option. One that should always be there for those like me who want it but to eliminate it or overprice it isn't going to make it better at all. It would make it worse. Microsoft's current business model is better than the traditional business model because it didn't work for three generations so why would they stay with it for a fourth generation? That would make no sense.

Like I said before, im giving Microsoft this entire generation to see how it all plays out. You can't pivot on a whim. You have to build it all up first and that in of itself takes time. Switching business models would only set them back further and makes things even worse than they already are.

Xbox has sucked for 20 years enough is enough.

Yep, a huge chunk of the posters are regulars from the Xbox subs.I heard horror stories about that place. A real xbox nest.

Sony vs Valve vs Nintendo just sounds so much better. MS won't be missed.Tbh, like I read from some people:

If MS gaming business is so reliant on this deal passing, it should go down in flames. They deserve to be obliterated.

Sony and Nintendo at least know what they're doing and both bounced back.

Why can't MS do it?

P

peter42O

Guest

Not everyone* Wants Xbox to "die"

Some like me just want them to spend the money they have investing in there own studios and using IP they have and IP they have not touched.

Build the studios up that they own, Give people a reason to want a Xbox and or GamePass.

It doesn't seem like that here at times because I read that more times than not.

They are building up the studios they own. They're doubling up the staff at Tango Gameworks based on Hi Fi Rush. Just because they're trying to acquire ABK (or whoever) doesn't mean that the building up studios is put on hold or something. They all take time to build up. Not like it can happen overnight.

I have like 10 reasons why I bought an Xbox and favor Game Pass. Everyone is different. What appeals to me may not appeal to you and vice versa.

Doesn't matter if they would do it or not. They have the money available. Foster studios, make partnerships. If Apple, Sony and Nintendo can do it, why can't MS?

What do you mean by partnerships though? I DON'T want Microsoft to pay for timed exclusivity for anything. I want them to stop doing that shit because it's a waste of money in my opinion. Also, they tried working with studios last generation and even accepted NOT owning the IP (Ryse, Quantum Break, etc.) and that didn't work out at all which is why Microsoft wants to OWN IP and I don't blame them. I would do exactly the same thing as would everyone else because why would you want to be reliant and dependent on these other companies for sequels, extra content, etc. when you can do it all yourself instead due to owning the IP?

You post is very clever and can be used to every Xbox generation.

So why they didn't change ever after 20 years?

Why do you keep giving Xbox one more chance? Again giving MS "this entrie generation to see how it all plays out".

MS don't want to lern and adapt to what the gaming market wants... they want to dominated it the easy way... buying their place without giving option for competition.

At least 20 years ago MS tried to release some games... today not even that anymore.

They just don't care about gaming.

It's valid for every generation because the leadership and CEO of Microsoft wasn't the same person. Everything changed with every generation. Look at 360 with Moore. Was great. Mattrick comes in, releases fucking Kinect and builds Xbox One completely around it which blew up in their face and he left before the console even launched.

I switched from PlayStation 4 to Xbox Series X as my primary gaming console. I went from NES/SNES to PS/PS2 to 360 to PS4 to XSX as my primary gaming console. I have always owned more than one console for every generation. The difference is that I only care about my primary. Whatever the secondary or tertiary consoles are doesn't matter all that much to me because they're always an exclusives only console so whatever is there, is there. Point being is as my primary gaming console this generation, Microsoft has this entire generation for me to either stay with them as my primary generation or I switch back to PlayStation which I did after 360.

I understand the point in regards to trying to dominate via buying but what exactly in gaming have they ever dominated? They've been 3rd every time. They're last on PC. They don't exist in mobile. So regardless of buying, they're nowhere near dominating anything and personally, I don't believe that they ever will because everything they do is interconnected so if you want to play Xbox games, you don't need a console, you can play on PC or mobile.

They don't care about gaming but have spent $80B in the last 5 years on their gaming division in order to build it up. Microsoft has released games this generation. Just because you or other don't like them or they're not for you doesn't mean that they didn't release games. They have. I don't care about Forza or Flight Sim and others but they still count.

One business is to make and sell or rent to users (and optionally play them in cloud gaming) videogames. The other business is offering to other corporations server space in their MS cloud and related services. Two very different business.How is it a separate unrelated business when Xbox is a division (not a subsidiary) and the only thing those two business divisions can have in common is servers?

We don't know how many MAU does Xbox cloud gaming has. GP should have 25-26M, a small portion of that should be GPU users and a small portion of that should be Xbox cloud gaming users. Pretty likely there are only a few, maybe a handful million Xbox cloud gaming MAU.Based on MAU alone, we're talking about millions of users moving from Google Cloud / AWS into Azure, and this doesn't even account for the future cloud gaming offering.

For the scale of Google Cloud or AWS this is nothing. And same goes for the future of cloud gaming, they are desperate spending almost $100B on gaming acquisitions because they aren't capable to compete against their direct competitors, who dominate them.

In this particular case, their direct competitor basically innovated becoming the first console maker on investing on cloud gaming, got all the cloud gaming patents, started the multigame subscripstions before them, built a bigger cloud gaming catalog, a bigger lineup of exclusives, got twice the subscribers that MS has and did it with a way more profitable business model for game subs/cloud gaming (not putting day one games there).

MS came later to make their own copy of these game subs and this cloud gaming, and has to make big acquisitions spending dozens of billions on acquisitions and almost give away super expensive AAA projects because aren't capable to build themselves a 1st party lineup as appealing as the Sony and MS one. And even doing that they can't compete at the same level.

No, it's a perfect equivalence, it's as nonsensical as your comparision.False equivalence and reduction ad absurdum?

MS has 60% of the cloud gaming market in UK, we don't know it's worldwide market share. We know that Sony has twice the game subbers than them.You really need to go back to school. No, Microsoft has an advantage because they already own >60% of the cloud gaming market, and have the second biggest cloud services provider in the world.

Having the 20% of the cloud server market and being top 2 isn't

relevant at all with their gaming/game subs/cloud gaming business. It can be seen knowing that Sony has more market share than MS+ABK combined and twice the game subs than MS without being in the cloud server market.

The acquisition has been blocked, so it won't happen. Unless MS has some way to appeal it in the court (not sure if possible) and wins the case.Acquiring ABK will not only further strength their cloud gaming marketshare, but do the same for their cloud service marketshare.

Having AB would help MS in cloud gaming a bit, or not. Becasuse it's a tiny, irrelevant market and will continue to be so in the future. And their direct competitor, where AB games are only a tiny portion of the games sold and rented there, makes way more money than them from game subs and have a way bigger amount of subscribers.

It's a nonsensical comparision, like yours. To make tvs doesn't benefit Sony in gaming and viceversa, in the same way that having server cloud services doesn't benefit MS in gaming/cloud gaming and viceversa.False equivalence. Even if it was a fair comparison, Sony is not in a leading market position for TV sales globally. In fact, they are 5th in a market dominated by Samsung.

TV, server clouds and gaming are separate business with basically no interconnection between them. And doesn't matter to have slightly cheaper tvs/server cloud because first they still have to pay most of their costs, second what they provide to the other business is a very tiny portion of their business, third what the other business provides/saves to gaming is to save a tiny portion of their total work/costs and could be perfectly made with other brands.

No, they are not.The costs are irrelevant.

Xbox Cloud gaming doesn't have 100M users at all. GP has around 25M, a portion of them are GPU users and a portion of the GPU users are Xbox Cloud gaming users and a portion of them are MAU. We don't know which are these portions, but pretty likely Xbox cloud gaming has only a handful million MAU being generous.Moving over 100 million users

MS doesn't dominate anything. They estimake a 60-70% cloud gaming market share for UK, not worldwide. Worldwide Sony has twice the game subs (game subs market is only 7-9% of the total gaming revenue), but we don't know the numbers for the tiny cloud gaming market (a small portion of the game subs market, so a tiny portion of the total gaming revenue).to their cloud offering + controlling even more of a market where they are already in a dominant position is the problem. Here, page 4.

This is data for the UK, which is the market that the CMA regulates and protects.The CMA has that data. Here, I'll help you if you have difficulties finding page 4 in the article above.

According to Newzoo, the UK generated in 2022 gaming consumer spending $5.5B (excluding hardware, b2b, gambling, taxes), which is almost a 3% of the $184.4B worldwide revenue. So it's a too small sample to consider it a reference for the global numbers, specially considering UK traditionally has been one of the few more pro-Xbox countries than the average.

Yes, I talk about worldwide because UK is only a tiny portion of the global revenue/total market. I know CMA only regulates/considers their own market and its numbers instead of the global ones, see my reply just above.Irrelevant. The UK makes decisions based on their market. You're the only one that keeps talking about worldwide, not me.

All of this is irrelevant. Market trends expect the cloud gaming market to almost exponentially grow in the next 10 years,

Your personal opinion is not market trends, it's an irrelevant personal opinion, like mine.That's not what market analysis says, and your opinion is irrelevant.

And no, as far as I know there is no serious market analysis that expects exponential growth for cloud gaming. And wouldn't make sense because there are external reasons that blocks it. And on top of that, if we look at the market trend (their performace in the previous years) its growth hasn't been exponential and there isn't any recent or future super important change that woud skyrocket them.

There isn't even an expected exponential growth even for the game subs (where cloud gaming is only a portion of them). Here's the most recent analysis I remember (optimistic but realistic because follows the trend of the previous years), where game subs are only expected to grow a 12% CAGR during the next 5 years, generating $17.9B in 2028. This is still under 10% of the current yearly total gaming revenue ($184.4B), which traditionally grows every year so in 2028 will be way higher.

This other market analysis, is older and more optimistic but still somewhat realistic. It says game subs generated $17.16 billion in 2021 and that will have a 2022 to 2031 12.9% CAGR, meaning they expect them to have the game subs generating $55.94B by 2031.

And well, there are many more in a similar fashion. Many estimating that game subs were a 7-9% of the total market and that in some years will grow to 15-16%.

As far as I know the only one that expects an unrealistic exponential growth for cloud gaming is maybe this one that having estimated $1.4B in 2021, they forecasted $2.4B for 2022 and $8.2B for 2028:

The explanation of why they went too aparently optimistic and unrealistic, to the point that it doesn't match their own forecasts for the gaming market revenue. The explanation is that in this graph they are also counting other things such as business to business solutions for gamedev studios / corporations, not final consumers/gamers, as you can see here in other slide of their research:

Ampere also had this other controversial market research, where claimed that GP was the market leader of game subs in the NA+EU market with a 60% market share, (but it was because for some reason they didn't include PS Plus in the related chart).

According to Ampere (not the first time they are controversial), the game subs revenue generated around $3.5B in the western markets instead of the $1.4B worldwide claimed by Newzoo (even incuded there B2B and other stuff) and from that they made this crazy chart with their forecast:

It's Ampere, so it's hard to take them seriously, but even they mention there "Download distribution dominance is clearly illustrated by Ampere’s consumer research which asks Xbox Game Pass Ultimate users how they access their games (see chart). Most usage is download-focused. As such, bucketing hybrid services such as Xbox Game Pass Ultimate and PlayStation Now into a cloud gaming market sizing is misleading and over-estimates the impact of this distribution technology in the near-term."

Cloud gaming isn't a nascent market, as I explained it's an over two decades old market that didn't have any important innovation in decades other than minor ones like tweaks to their codecs or gamepads to reduce a bit latency.and market based decisions are made from those assumptions. It's a nascent market - You should look up what it means.

It's a small market that can't scale to go mainstream due to several constrains that the related companies can't address such as the laws of physics, related bandwidth and electricity costs, good internet connection quailty/prices/data caps/wifi and cable standards, and many more.

The market share of the one who buys and the one acquired for that market (gaming) is relevant.This is all irrelevant. The CMA dropped their concerns about a console SLC. Microsoft owning 60 to 70% of the cloud gaming market + the 2nd biggest cloud services is the problem. They are a market leader in a nascent market + they would be able to move hundreds of millions of users to their cloud services provider.

In the same way that it's relevant how the acquired company impacts in the main gaming business (console market) of the direct competitor of the acquirer. Specially if you also want to estimate the potential impact that the acquisition on a very small subset of this market (cloud gaming market inside game sub market inside console gaming market).

MS is not a worldwide leader in any gaming market. They have an 'estimated (estimated by who knows who, but let's hope it's real) 60-70% cloud gaming market share' in UK, that's all. And the cloud gaming market is tiny and irrelevant, not nascent.Are you so narrow minded that you think a company being the leader on a nascent market that involves CLOUD SERVERS, while being the second biggest in a market that also involves CLOUD SERVERS, is the same as comparing Teslas to Bananas? You really are hopeless.

Maybe not to Teslas and bananas, but it's like saying that gamedevs listen music and since Sony has a good position in the music market it gives them an advantage on the gamedev market. It's something stupid and nonsensical.

Avoid insulting who disagrees with you, it only makes you look pathetic and embarassing.You seem to be very well acquainted with whatever Xbox bullshit is out there. Must be in your nightstand, right next to the phil spencer dildo.

Last edited:

Or worst the PC subsYep, a huge chunk of the posters are regulars from the Xbox subs.

Thats a lot of text, i know some of you are butthurt by this result, but have some decency and self awarenessOne business is to make and sell or rent to users (and optionally play them in cloud gaming) videogames. The other business is offering to other corporations server space in their MS cloud and related services. Two very different business.

We don't know how many MAU does Xbox cloud gaming has. GP should have 25-26M, a small portion of that should be GPU users and a small portion of that should be Xbox cloud gaming users. Pretty likely there are only a few, maybe a handful million Xbox cloud gaming MAU.

For the scale of Google Cloud or AWS this is nothing. And same goes for the future of cloud gaming, they are desperate spending almost $100B on gaming acquisitions because they aren't capable to compete against their direct competitors, who dominate them.

In this particular case, their direct competitor basically innovated becoming the first console maker on investing on cloud gaming, got all the cloud gaming patents, started the multigame subscripstions before them, built a bigger cloud gaming catalog, a bigger lineup of exclusives, got twice the subscribers that MS has and did it with a way more profitable business model for game subs/cloud gaming (not putting day one games there).

MS came later to make their own copy of these game subs and this cloud gaming, and has to make big acquisitions spending dozens of billions on acquisitions and almost give away super expensive AAA projects because aren't capable to build themselves a 1st party lineup as appealing as the Sony and MS one. And even doing that they can't compete at the same level.

No, it's a perfect equivalence, it's as nonsensical as your comparision.

MS has 60% of the cloud gaming market in UK, we don't know it's worldwide market share. We know that Sony has twice the game subbers than them.

Having the 20% of the cloud server market and being top 2 isn't

relevant at all with their gaming/game subs/cloud gaming business. It can be seen knowing that Sony has more market share than MS+ABK combined and twice the game subs than MS without being in the cloud server market.

The acquisition has been blocked, so it won't happen. Unless MS has some way to appeal it in the court (not sure if possible) and wins the case.

Having AB would help MS in cloud gaming a bit, or not. Becasuse it's a tiny, irrelevant market and will continue to be so in the future. And their direct competitor, where AB games are only a tiny portion of the games sold and rented there, makes way more money than them from game subs and have a way bigger amount of subscribers.

It's a nonsensical comparision, like yours. To make tvs doesn't benefit Sony in gaming and viceversa, in the same way that having server cloud services doesn't benefit MS in gaming/cloud gaming and viceversa.

TV, server clouds and gaming are separate business with basically no interconnection between them. And doesn't matter to have slightly cheaper tvs/server cloud because first they still have to pay most of their costs, second what they provide to the other business is a very tiny portion of their business, third what the other business provides/saves to gaming is to save a tiny portion of their total work/costs and could be perfectly made with other brands.

No, they are not.

Xbox Cloud gaming doesn't have 100M users at all. GP has around 25M, a portion of them are GPU users and a portion of the GPU users are Xbox Cloud gaming users and a portion of them are MAU. We don't know which are these portions, but pretty likely Xbox cloud gaming has only a handful million MAU being generous.

MS doesn't dominate anything. They estimake a 60-70% cloud gaming market share for UK, not worldwide. Worldwide Sony has twice the game subs (game subs market is only 7-9% of the total gaming revenue), but we don't know the numbers for the tiny cloud gaming market (a small portion of the game subs market, so a tiny portion of the total gaming revenue).

This is data for the UK, which is the market that the CMA regulates and protects.

According to Newzoo, the UK generated in 2022 gaming consumer spending $5.5B (excluding hardware, b2b, gambling, taxes), which is almost a 3% of the $184.4B worldwide revenue. So it's a too small sample to consider it a reference for the global numbers, specially considering UK traditionally has been one of the few more pro-Xbox countries than the average.

Yes, I talk about worldwide because UK is only a tiny portion of the global revenue/total market. I know CMA only regulates/considers their own market and its numbers instead of the global ones, see my reply just above.

Your personal opinion is not market trends, it's an irrelevant personal opinion, like mine.

And no, as far as I know there is no serious market analysis that expects exponential growth for cloud gaming. And wouldn't make sense because there are external reasons that blocks it. And on top of that, if we look at the market trend (their performace in the previous years) its growth hasn't been exponential and there isn't any recent or future super important change that woud skyrocket them.

There isn't even an expected exponential growth even for the game subs (where cloud gaming is only a portion of them). Here's the most recent analysis I remember (optimistic but realistic because follows the trend of the previous years), where game subs are only expected to grow a 12% CAGR during the next 5 years, generating $17.9B in 2028. This is still under 10% of the current yearly total gaming revenue ($184.4B), which traditionally grows every year so in 2028 will be way higher.

This other market analysis, is older and more optimistic but still somewhat realistic. It says game subs generated $17.16 billion in 2021 and that will have a 2022 to 2031 12.9% CAGR, meaning they expect them to have the game subs generating $55.94B by 2031.

And well, there are many more in a similar fashion. Many estimating that game subs were a 7-9% of the total market and that in some years will grow to 15-16%.

As far as I know the only one that expects an unrealistic exponential growth for cloud gaming is maybe this one that having estimated $1.4B in 2021, they forecasted $2.4B for 2022 and $8.2B for 2028:

The explanation of why they went too aparently optimistic and unrealistic, to the point that it doesn't match their own forecasts for the gaming market revenue. The explanation is that in this graph they are also counting other things such as business to business solutions for gamedev studios / corporations, not final consumers/gamers, as you can see here in other slide of their research:

Ampere also had this other controversial market research, where claimed that GP was the market leader of game subs in the NA+EU market with a 60% market share, (but it was because for some reason they didn't include PS Plus in the related chart).

According to Ampere (not the first time they are controversial), the game subs revenue generated around $3.5B in the western markets instead of the $1.4B worldwide claimed by Newzoo (even incuded there B2B and other stuff) and from that they made this crazy chart with their forecast:

It's Ampere, so it's hard to take them seriously, but even they mention there "Download distribution dominance is clearly illustrated by Ampere’s consumer research which asks Xbox Game Pass Ultimate users how they access their games (see chart). Most usage is download-focused. As such, bucketing hybrid services such as Xbox Game Pass Ultimate and PlayStation Now into a cloud gaming market sizing is misleading and over-estimates the impact of this distribution technology in the near-term."

Cloud gaming isn't a nascent market, as I explained it's an over two decades old market that didn't have any important innovation in decades other than minor ones like tweaks to their codecs or gamepads to reduce a bit latency.

It's a small market that can't scale to go mainstream due to several constrains that the related companies can't address such as the laws of physics, related bandwidth and electricity costs, good internet connection quailty/prices/data caps/wifi and cable standards, and many more.

The market share of the one who buys and the one acquired for that market (gaming) is relevant.

In the same way that it's relevant how the acquired company impacts in the main gaming business (console market) of the direct competitor of the acquirer. Specially if you also want to estimate the potential impact that the acquisition on a very small subset of this market (cloud gaming market inside game sub market inside console gaming market).

MS is not a worldwide leader in any gaming market. They have an 'estimated (estimated by who knows who, but let's hope it's real) 60-70% cloud gaming market share' in UK, that's all. And the cloud gaming market is tiny and irrelevant, not nascent.

Maybe not to Teslas and bananas, but it's like saying that gamedevs listen music and since Sony has a good position in the music market it gives them an advantage on the gamedev market. It's something stupid and nonsensical.

Avoid insulting and crying, it only makes you look pathetic and embarassing.

Let us take a moment to thank Google for failing with Stadia, because if they had succeeded, MS would've bought ABK.

Thanks, Google!

Thanks, Google!

I don't want Microsoft to die, but I do want them to stop trying to actively fuck me and my gaming experiences.It doesn't seem like that here at times because I read that more times than not.

As @TubzGaming said, focus on building their studios up from the ground.

I hate the fact that their philosophy seems to be for a better use of words " To rob Peter to pay Paul" as in taking away a beloved franchise from a group of gamers only to say "look how awesome we are guys." as they give said games to their base.

I hope you can see that.

Last edited:

We already don’t like it.Passive aggressive walls of text, flashing around conceptual dildos... what is going on here?

You don't want to make me angry. You won't like it.

Dude its for fun. At least for me. Yea its no different. But i see people so much invested in toys and plastic box its nuts (mostly xbox fans and online personas).Everyone here wants Xbox to die so how is me saying that Microsoft should buy Sony any fucking different?

But that is why they are in 3rd (and probaly even lower if it has others players)... because they don't care and invest in games.It doesn't seem like that here at times because I read that more times than not.

They are building up the studios they own. They're doubling up the staff at Tango Gameworks based on Hi Fi Rush. Just because they're trying to acquire ABK (or whoever) doesn't mean that the building up studios is put on hold or something. They all take time to build up. Not like it can happen overnight.

I have like 10 reasons why I bought an Xbox and favor Game Pass. Everyone is different. What appeals to me may not appeal to you and vice versa.

What do you mean by partnerships though? I DON'T want Microsoft to pay for timed exclusivity for anything. I want them to stop doing that shit because it's a waste of money in my opinion. Also, they tried working with studios last generation and even accepted NOT owning the IP (Ryse, Quantum Break, etc.) and that didn't work out at all which is why Microsoft wants to OWN IP and I don't blame them. I would do exactly the same thing as would everyone else because why would you want to be reliant and dependent on these other companies for sequels, extra content, etc. when you can do it all yourself instead due to owning the IP?

It's valid for every generation because the leadership and CEO of Microsoft wasn't the same person. Everything changed with every generation. Look at 360 with Moore. Was great. Mattrick comes in, releases fucking Kinect and builds Xbox One completely around it which blew up in their face and he left before the console even launched.

I switched from PlayStation 4 to Xbox Series X as my primary gaming console. I went from NES/SNES to PS/PS2 to 360 to PS4 to XSX as my primary gaming console. I have always owned more than one console for every generation. The difference is that I only care about my primary. Whatever the secondary or tertiary consoles are doesn't matter all that much to me because they're always an exclusives only console so whatever is there, is there. Point being is as my primary gaming console this generation, Microsoft has this entire generation for me to either stay with them as my primary generation or I switch back to PlayStation which I did after 360.

I understand the point in regards to trying to dominate via buying but what exactly in gaming have they ever dominated? They've been 3rd every time. They're last on PC. They don't exist in mobile. So regardless of buying, they're nowhere near dominating anything and personally, I don't believe that they ever will because everything they do is interconnected so if you want to play Xbox games, you don't need a console, you can play on PC or mobile.

They don't care about gaming but have spent $80B in the last 5 years on their gaming division in order to build it up. Microsoft has released games this generation. Just because you or other don't like them or they're not for you doesn't mean that they didn't release games. They have. I don't care about Forza or Flight Sim and others but they still count.

You can't have a platform and release a game each few years... that doesn't works.

And maybe you are having a revisionist history here because Kinect was what hold and make 360 reach over 84 million units sold.

After Kinect 360 had a boom in sales... so 2010, 2011 and 2012 was really something odd in terms of sales for a 6 year console.

If not Kinect then 360 should have stopped at around 60 million and PS3 confortable passing it after 2010.

You guys blame Kinect but it was what made 360 reach where it was.

2011: 55m 360 / 10m Kinects

2012: 66m 360 / 18m Kinects

Do you understand when you look at NPD data (the strongest 360 region) you see that?

Kinect was the reason 360 shined.

Xbox One? You blame Dom Mattrick and Kinect but in fact it was already the same Xbox team that you see today... and the issue with Xbox One was not Kinect... it was being underpowered compared to PS4 but costing $100 more.

If Xbox One had a hardware similar to PS4 and costing $399 it should do way better than what it id.

And to be fair it did better than Series is doing.

You guys keep blaming the wrong reasons with revisionist histories.

Games is what MS needs and they fail to delivery every single generation... where generation you keep asking why MS stopped to release games

The difference is that now in Series case they are not even trying anymore.

I don't want Xbox die... I want MS to continue to doing that "competition" to rest of my life